In a previous post, I discussed the basics of the compliance environment and some proactive measures that can be taken to stay ahead of the storm; now, let’s refresh your memory. Take out your checklists: How is your company faring toward compliance as we head into the calendar year-end?

In a previous post, I discussed the basics of the compliance environment and some proactive measures that can be taken to stay ahead of the storm; now, let’s refresh your memory. Take out your checklists: How is your company faring toward compliance as we head into the calendar year-end?

Checklist Reminders:

- You’ve gauged your company’s tolerance for risk and weighted it against your workforce mix.

- You’ve designed, or better yet, amended your policies to reflect not only your company’s standards and procedures for utilization of contingent workers, but specifically how independent contractors and outsourced service providers are vetted and validated.

- You’ve made Accounts Payable and Facilities your best friends, and you’ve combed through the data to have a better understanding of your current populations at risk.

I promised to share some common — and not-so-common — audit triggers that should be avoided at all costs. First, we’ll look at these triggers with a more myopic lens. Next, I’ll dive into actions that can be taken to prevent the things you fear most for yourselves and your organizations. Last, I’ll close this post and tie it up in a bow. This is the “gift in disguise” component.

PREMIUM CONTENT: Non-Traditional Contract Clauses for the Contingent Workforce Manager

Federal and State-Level Triggers for Audits

There is no denying that the compliance process is complex because there is not one defined standard but multiple factors that come into consideration across various levels of government — what one agency accepts, another agency rebukes. Because knowing is half the battle, arm yourself to be aware of the most common triggers for audits, including:

- A W-2 and 1099 issued for the same worker by the same company in the same fiscal year — this could occur when an independent contractor is converted to a direct hire or when a former employee is brought back as an independent contractor;

- All tax audits by the government are now requiring a 1099 audit also be conducted;

- Unemployment or Workers’ Compensation claims;

- Formal request for the determination of worker status (IRS Form SS-8) — this formal request asks the IRS to give a determination as to whether the services being provided are that of an employee or independent contractor;

- State-level requirements not being met — in particular, the 12 “hot” states that have additional New Hire reporting requirements for Child Welfare enforcement initiatives.

- Information Sharing Agreements — often times this can create a “snowball” effect where one audit will trigger another; and

- Tips from competitors and/or disgruntled employees

Preventative Medicine You Must Take!

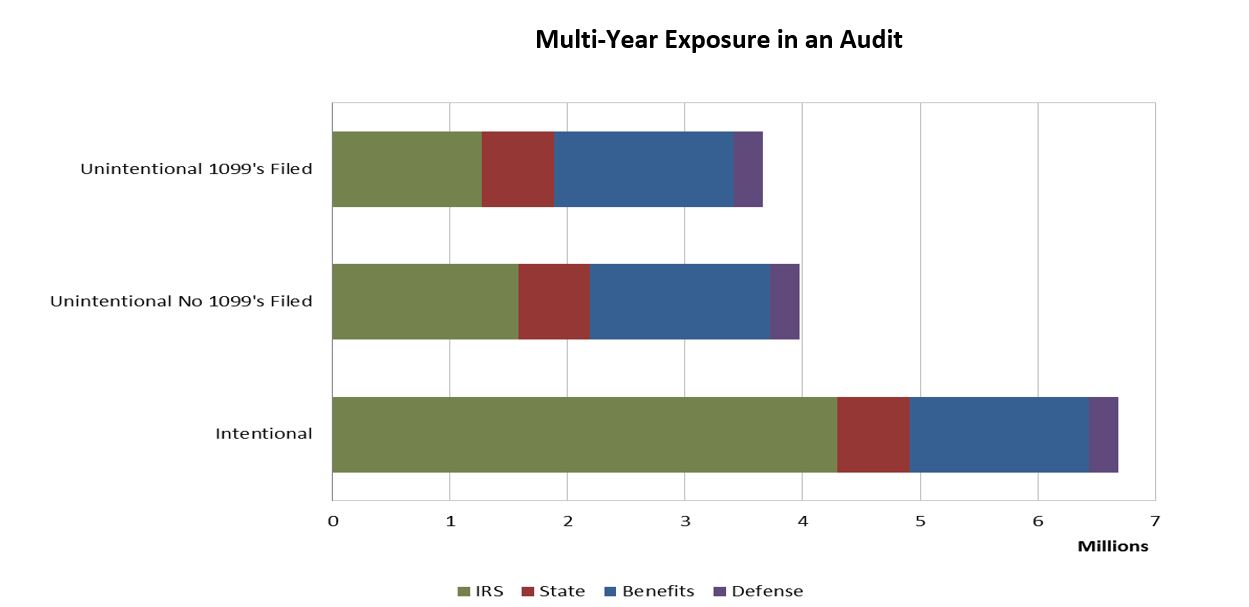

Now, you have the makings of an action plan and you are ready to go into the New Year in a more “compliance-ready” state of mind. To guard against the tipping point of one or more triggers happening right under your nose, your company should conduct a risk assessment. Risk assessments can come in many flavors from minimalistic, where a shallow examination is conducted across a few areas, to holistic, where an organization’s entire contingent workforce program is reviewed. Review your organization’s tolerance for risk and your total workforce mix in order to create a balanced approach. An additional index in the equation is price; however, price is not the most significant measure — the most significant measure is cost. Consider the numbers:

Having examined your organization’s level of risk aversion and the total workforce mix, and weighing this against your company’s appetite for cost, you are ready to socialize your findings with senior leaders within your organization. The ability to have that tough conversation — and provide proactive recommendations — is the “gift.” In all “Best in Class” companies, leaders and employees have one thing in common…they want to do the right thing. The best way to do that is to provide data and evidentiary points of reference to what’s at stake here coupled with some best practices for navigating higher risk areas.

Next time I revisit the topic of the Compliance Continuum™, I’ll share the most common myths that need to be dispelled in order to really protect your company and your key talent. Hint: Just because you vet and validate your riskiest talent pools, does not mean that you’ve solved the entire equation.

MORE: Ensuring compliance for your independent contractors

[…] Dana Shaw, published in Staffing Industry Analysts’ “Staffing Stream.” Read: Unintended Consequences Along the Compliance Continuum (TM) Part II: 2014 Audit Proofing Advice to learn about the common–and not so common–audit triggers and proactive measures that […]